Confident investors undeterred by rate hikes

It had been eleven years since the Reserve Bank of Australia last raised the Australian cash rate (a historic 137 months, to be precise), but in May 2022 the cash rate was raised 25 basis points. This was closely followed by three consecutive monthly increases.

Inflation has continued to be a problem in 2022 so further rate increments are expected, with some forecasting the cash rate could sit at around 2.35 per cent by the end of 2022.

The ramification for property owners is that the cost of borrowing is now more expensive. The sheer volume of media around rate hikes this year has been quite extraordinary, with the narrative causing fear for many of the estimated 1.1 million Australian mortgage holders who have never experienced an increase in interest rates, and for those looking to enter the market.

After a period of persistent growth, the Australian property market is cooling off in most areas with property prices in some metro areas correcting at rates not seen for some time. Consumer sentiment has fallen and demand for housing credit is expected to slow, putting further downward pressure on growth rates. Lenders have already tightened assessment criteria with increased interest rate buffers; some people will find it harder to get finance.

While it may all sound like doom and gloom, the forecast for property investors is looking more promising. Not only is there now more certainty around many of the issues that have been holding investors back over the past few years such as the effect of COVID-19 on immigration and the impact of a change in government, but rental rates and yields have been increasing.

According to CoreLogic, “Unlike changes in dwelling purchase values, rental value growth remains high across Australian dwellings. Rent values increased a further 0.9% in June, taking rents 9.5% higher over the year.”

Nationally, investor finance made up 35.8% of new mortgage lending through the month of April, up from 26.1% twelve months ago, and above the decade average of 34.8%.

Considering this and all the tax deductions available to investors — interest, depreciation, repairs, maintenance and insurance to name a few — the outlook is looking favourable for investors. Given that interest is the largest tax deduction available for property investors, the impact of interest rate increases is not felt as harshly as it is for first homeowners and owner occupiers.

In fact, investors will likely see the slowing of owner-occupier activity as an opportunity to invest as property prices stabilise and rental yields remain strong. At BMT we wouldn’t be surprised to see an emerging property market dominated by investors, similar to what Australia experienced in the year following the Global Financial Crisis.

In the following case study, we demonstrate how a 1 per cent interest rate increase has a reduced effect on the cash flow of a property investor versus that of an owner occupier.

Case study

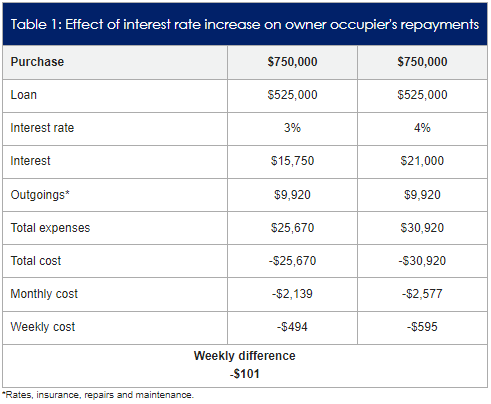

To keep things simple, we have kept the variables the same for both the owner-occupier and the investor. We have assumed that both have a loan of $525,000 with a 5-year interest-only period on a townhouse purchased for $750,000.

Table 1 shows the general impact of the increase in interest rates on cash flow. A one per cent increase in interest would translate into an ex

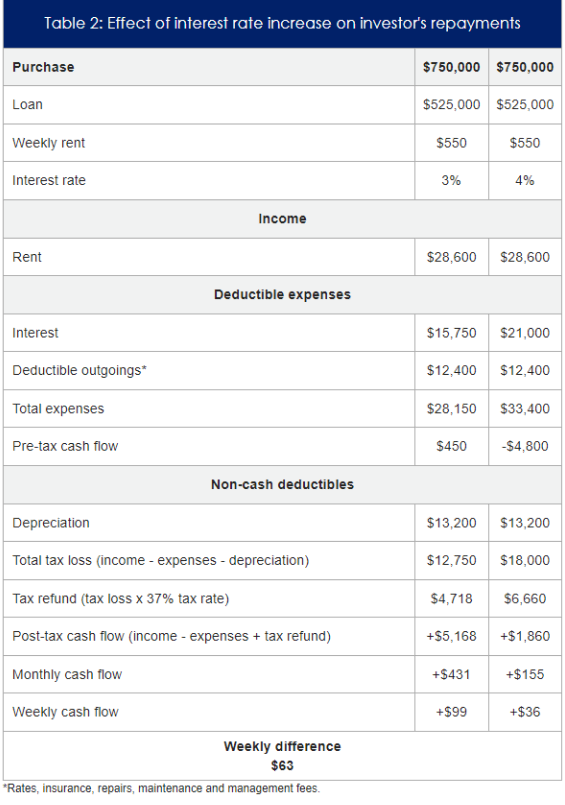

The full impact of the rate increase will be felt by the owner-occupier since there are no available associated tax deductions to soften the effect. But let’s see what happens to the investor’s cash flow (Table 2).

Factoring in the tax deductibility of the interest lessens the impact for the landlord, who will only feel a difference of $63 per week – and in this scenario still be cash flow positive – compared to the extra $101 hit for the owner-occupier who will end up more than $500 out of pocket.

Savvy investors will crunch the numbers using PropCalc, BMT’s free investment property affordability calculator. PropCalc provides a realistic breakdown of the cost of owning any property. PropCalc allows users to customise their income, property expenses – and to model out the impact of changing interest rates on affordability.

This article first appeared in BMT Quantity Surveyors.

{kind=link}