When you’re planning out your investing strategy, one of the first aspects to consider is the number of properties you need or want. Without spending hours crunching through detailed spreadsheets, how do you work this out efficiently?

Just one first thanks

Some people we work with would just be happy to buy their first property. But once you have done that, the prospect of buying ‘a few’ more starts to become a reality.

A basic starting point we use is to think about the annual income you are targeting – for example $100,000. Next, we work out how many properties would deliver this income.

Baseline

In planning, we need to use some assumptions and a baseline. In order to model the number of properties required to achieve the target income, we use the weekly rental income per property, and work this out on 50 weeks per year. Using 50 weeks per year provides a small buffer for vacancy periods.

We have also included a base of $6,000 per year to cover costs of property management, insurance and potential repairs . . yes, this fee could look small in some years but we have to start somewhere.

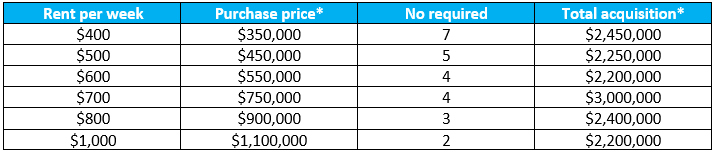

Using this approach provides us with information about the number of properties required to achieve the total rental target, and also demonstrates the variables involved in meeting the target. That is, seven properties will deliver the target annual income of $98,000 at the lower end of the scale, while only two are required at the higher rental amount.

Of course, many of our clients are targeting a much bigger annual income so the table above covers three key levels $100,000, $200,000 and $500,000.

Cost to purchase

The next step is quite difficult to model, so please note we are making quite broad assumptions in relation to purchase prices.

* Assuming your strategy is to purchase positive cash flow properties – note that rent is not always proportional to acquisition price.

We’re assuming here that a property achieving a rental income of $400 per week will cost less to purchase than a property achieving a rental income of $600 per week. This is definitely not a rule, but the table above demonstrates the importance of acquisition price in relation to the rental amount.

There are many other variables to consider, not the least of which is your ability to increase a property’s rent through renovation or mini-development, and many ways to purchase at a range of price points. If rent was proportional to the purchase price, as it is in the table above, then you would achieve your target rental income for a lower total acquisition price. This news surprises some people when we work through their planning.

Antiseptic life

What shame real life is not like living in a model. It would be great for investment predictability. But real life is not as predictable as our model, and for this reason your plans need to be revised with each purchase you make.

Along with the realities of purchasing in an active market, our model has not taken into account the challenges of purchasing properties in particular price brackets, or tax and the variabilities of other acquisition costs such as stamp duty, maintenance, insurance and rates. However, it provides a framework for planning and allows us to move towards the end game . . .that is, how do you ‘own’ the properties or pay down the loans.

Pay it off

For the purposes of providing a succinct overview, we have not covered the quite crucial step of explaining how to leverage one property to purchase more, as this is addressed in detail in our other publications. So, to stay on topic, outlined below are just a few of the ways you might use to achieve the goal of earning $100,000 or your target income outright.

- Buy very well = less to pay off.

- Buy and let capital growth and rental increases pay the loan repayments over time.

- Combine the excess rents (in a positive cash flow portfolio) to pay one property off at a time (or just pay the offset to the minimum amount . .see my note below).

- Use projects to fast track your repayments – for example, buy a property to renovate and sell or split in half and sell the back block.

- Buy more than you plan to keep, wait for capital growth then sell the most strategically beneficial property/ies.

- Renovate to increase rents.

- Develop some properties to facilitate wholesale purchases – for example, develop townhouses to replace a house on a single lot

NOTE : It wouldn’t be a Property Frontline blog if I didn’t add a little extra point at the end. The best case scenario would be to use good loan structures so you have an offset facility attached to your portfolio, with the aim of not completely paying off the loan entirely. But . .you would need to speak to a good mortgage broker who could advise you on the best way to manage your specific requirements.

About the author

Debra Beck-Mewing is the Editor of the Property Portfolio Magazine and CEO of The Property Frontline. She has more than 20 years’ experience in buying property Australia-wide and has extensive experience in helping buyers use a range of strategies including renovating, granny flats, sub-division and development. Debra is a skilled property strategist, and a master in identifying tailored opportunities, homes and sourcing properties that have multiple uses. She is a Qualified Property Investment Advisor, licensed real estate agent and also holds a Bachelor of Commerce and Master of Business. As a passionate advocate for increasing transparency in the property and wealth industries, Debra is a popular speaker on these topics. She is also an author, podcast host, and participates on numerous committees including the Property Owners’ Association.

Follow us on facebook.com/ThePropertyFrontline for regular updates, or book in for a strategy session to discuss your property questions.

Disclaimer – This information is of a general nature only and does not constitute professional advice. We strongly recommend you seek your own professional advice in relation to your particular circumstances.

{kind=link}